Some have argued that peer-to-peer insurance should be like peer-to-peer lending, i.e. creating a market place where the buyer and sellers of loans can come together, or in the case of insurance, a market place where the buyer and sellers of insurance risk can come together.

But is a new market place really being made? Assessing credit risk and then securitising the loans so investors can buy them is nothing new. Banks have been securitising loans for many years now e.g. mortgage-backed securities. Arguably banks are performing an additional service of diversifying the loans first which peer-to-peer lenders do not do.

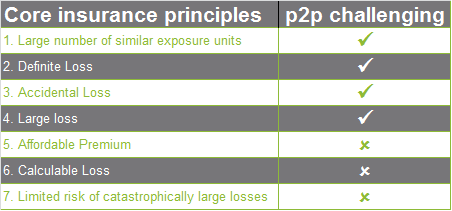

Insurers too are not new to securitisation, 'insurance transformers' have been around for a while. Interestingly, the marketability of securitised insurance risk is normally limited to catastrophic risks - normally because of the complex influence of underwriters and difficult to compare terms and conditions.

For both securitised loans and securitised insurance risk, buyers tend to be highly sophisticated i.e. hedge and pension funds, other banks or insurers. In fact, it was only when ‘the crowd’ such as local municipalities starting investing in these types of securities that things started going wrong i.e. the GFC. So these models have don't favour micropreneurs.

So should these market places be called ‘sophisticated buyers’-to-peer loans or insurance instead of peer-to-peer, maybe peer-to-peer is something else, or as Forrest Gump says - maybe it’s both.

But is a new market place really being made? Assessing credit risk and then securitising the loans so investors can buy them is nothing new. Banks have been securitising loans for many years now e.g. mortgage-backed securities. Arguably banks are performing an additional service of diversifying the loans first which peer-to-peer lenders do not do.

Insurers too are not new to securitisation, 'insurance transformers' have been around for a while. Interestingly, the marketability of securitised insurance risk is normally limited to catastrophic risks - normally because of the complex influence of underwriters and difficult to compare terms and conditions.

For both securitised loans and securitised insurance risk, buyers tend to be highly sophisticated i.e. hedge and pension funds, other banks or insurers. In fact, it was only when ‘the crowd’ such as local municipalities starting investing in these types of securities that things started going wrong i.e. the GFC. So these models have don't favour micropreneurs.

So should these market places be called ‘sophisticated buyers’-to-peer loans or insurance instead of peer-to-peer, maybe peer-to-peer is something else, or as Forrest Gump says - maybe it’s both.